What is in vitro diagnostics (IVD)? The FDA definition of IVD encompasses reagents, instruments, and systems intended for diagnosis of disease.

The market covers almost all indications and is a vital component of healthcare. As a result, it contains several mature markets that are now being driven primarily by an increasing population base, but it is also being disrupted by new technologies such as point of care testing and genetic testing.

Access deeper industry intelligence

Experience unmatched clarity with a single platform that combines unique data, AI, and human expertise.

The key drivers of the IVD market are an aging population and rising rates of obesity and chronic disease globally, driving increased use of regular diagnostic testing. In IVD, much of the testing is performed by traditional techniques that have been used for many years, such as immunoassays, which are still utilised heavily. However, increased use of molecular testing is driving growth, particularly in infectious disease. Additionally, uptake of point of care molecular testing is driving growth in several markets as technology has improved.

One barrier to growth has been significant pricing pressures, both from high levels of competition and reimbursement policies. Europe has been particularly affected by competitive pricing pressures, which has limited growth despite an increased number of tests being performed. While novel biomarkers are driving growth in some markets, one particular example being procalcitonin, there has been low uptake of many novel biomarkers, such as copeptin and ST2, which have seen very low adoption despite data showing strong evidence of utility. This mixed uptake of novel biomarkers is limiting growth in new markets.

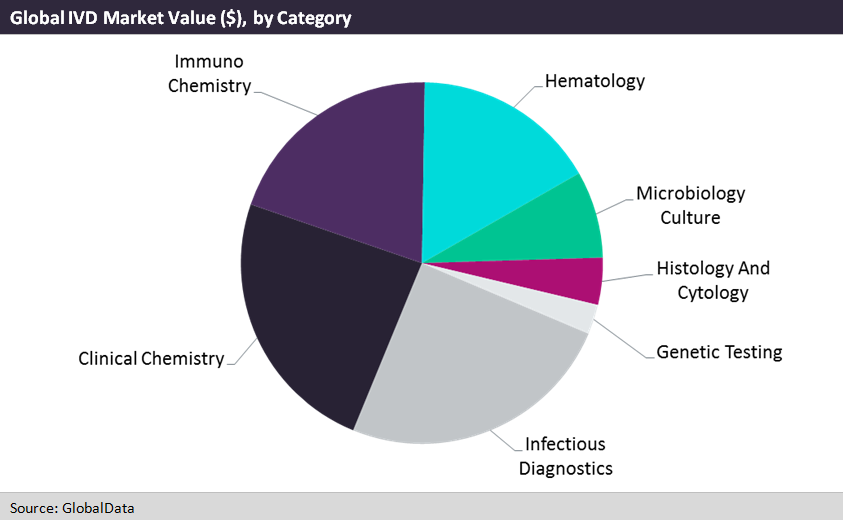

The overall market value of IVD is $52B this year, and is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.2% to $69B in 2024. The largest market is infectious diagnostics, valued at $12.9B, closely followed by clinical chemistry, as shown in the figure below.

US Tariffs are shifting - will you react or anticipate?

Don’t let policy changes catch you off guard. Stay proactive with real-time data and expert analysis.

By GlobalDataIn recent years, there has been a continuing trend towards lab consolidation, with hospitals forming networks to perform tests with high throughput and lower overhead costs. This trend is expected to continue in the future, requiring labs to look for scalability in their analysers. Companies are adapting to this trend by offering modular analysers, seen in Roche’s Cobas series, Abbott’s Alinity analysers, and Siemens’ Atellica Solution, for example. Automated analysers are expected to grow at a much faster rate than semi-automated analysers, which are analysers requiring some manual intervention during testing. However, our research indicates that the semi-automated analysers will still be increasing in market value through to 2024. The driver for this is primarily from replacement sales to low-throughput laboratories that do not yet feel the need to move to an automated analyser.

The fastest area of growth is in the new digital polymerase chain reaction (PCR) systems. Digital PCR builds on traditional PCR amplification and fluorescent probe–based detection methods to provide highly sensitive absolute quantification of nucleic acids without the need for standard curves. This is a new approach to nucleic acid detection and quantification, which involves a different method of absolute quantification and rare allele detection relative to conventional PCR, because it directly counts the number of target molecules rather than relying on reference standards or endogenous controls. The market is growing at an astounding CAGR of 10.5% and will see more growth as it becomes the industry standard.

Additionally, point of care technology has improved in recent years. GlobalData has observed a shift in physicians’ attitudes towards viewing point of care tests as a reliable alternative to laboratory testing, whereas previously there was significant concern about the quality of these tests. While there is still some resistance, it does seem to be decreasing, particularly with the advent of high sensitivity troponin testing. However, there is still significant resistance that arises from the nature of point of care testing itself. It is a fundamentally disruptive technology, which requires a reorganisation of the healthcare setting in order to be implemented. This resistance has been particularly prominent in France, which has a much lower POC market value than would otherwise be expected. To overcome this, companies need to focus on finding champions within organisations who are willing to push for point of care technologies, far more so than with other tests.

Overall, GlobalData expects to see continued growth in the IVD market, predominantly driven by rising prevalence of diseases and the adoption of new technologies. A continued effort to overcome resistance to new biomarkers or technologies is vital for companies looking to expand their product offerings.